A Radical New Idea for a Frozen Market

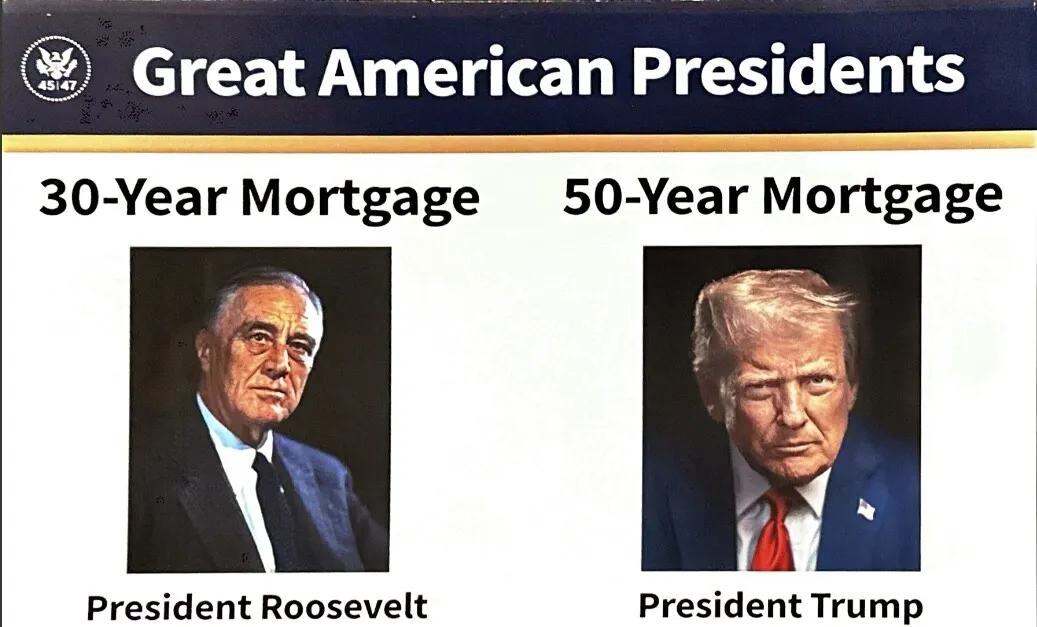

The Trump administration is reportedly exploring the creation of a 50-year mortgage, a bold attempt to break the deadlock in America’s housing market by extending the repayment horizon and lowering monthly costs for buyers squeezed by high interest rates.

According to officials familiar with the discussions, the plan is being developed as part of a broader housing affordability initiative set to be unveiled later this year. The White House sees the ultra-long-term mortgage as a potential lever to revive home sales, expand access for first-time buyers, and relieve pressure on the construction industry.

“We’re in a housing affordability crisis,” said a senior administration official. “People can’t buy, builders can’t build, and lenders can’t lend. Extending the term of the mortgage is one way to unlock movement again.”

Why the 30-Year Mortgage No Longer Works

For decades, the 30-year fixed-rate mortgage has been the cornerstone of the American housing market. But after years of rising prices and elevated borrowing costs, the traditional model has become too restrictive for many.

With average mortgage rates hovering around 6.5%, the monthly payment on a median-priced home has increased nearly 70% since 2020, according to data from Redfin.

“The 30-year mortgage has hit its limit,” said Mark Fleming, chief economist at First American Financial. “Affordability has collapsed, and unless incomes double or rates drop dramatically, the math just doesn’t work for most households.”

A 50-year term, officials argue, could reduce monthly payments by roughly 20–25%, depending on the interest rate, helping to bring millions of sidelined buyers back into the market.

A Lifeline, or a Long-Term Trap?

Critics warn the proposal could come with serious long-term risks. A 50-year mortgage would dramatically increase total interest paid over the life of the loan and could trap homeowners in decades of debt with little equity gain early on.

“It’s a short-term fix that creates long-term problems,” said Diane Swonk, chief economist at KPMG. “It might boost demand, but it won’t solve the underlying supply issue or rising construction costs.”

Still, proponents argue that with housing inventory near record lows and millions priced out, bold measures are necessary. The administration is reportedly considering safeguards such as prepayment flexibility and lower early-term interest rates to make the loans more manageable.

The Political and Economic Context

The push for longer mortgage terms comes amid intense pressure on the Trump White House to tackle housing affordability ahead of the 2026 midterms.

Soaring property values, limited supply, and high rates have combined to freeze the market. Existing home sales have fallen to their lowest level in nearly 30 years, and new housing starts have slowed sharply despite strong demand.

Economists say a 50-year option could stimulate construction by unlocking new financing demand, though some warn it could also inflate prices further if not paired with policies to expand supply.

“This could make mortgages cheaper but homes more expensive,” said Fleming. “Unless zoning and labor constraints are addressed, you’re just shifting the problem.”

International Precedents

Ultra-long-term mortgages aren’t new globally. Japan and parts of Europe have experimented with 50-year and even 100-year loans, often tied to intergenerational ownership structures.

In Japan, 50-year mortgages emerged during the 1980s real estate boom, allowing families to pass debt to their heirs. However, critics note the model also contributed to asset bubbles and prolonged household leverage.

“The U.S. market is different,” Swonk said. “But history shows stretching credit too far can have unintended consequences.”

Wall Street’s Early Reaction

Financial markets initially reacted positively to reports of the proposal, with homebuilder and mortgage lender stocks rising in early trading. Shares of Lennar, D.R. Horton, and Rocket Mortgage all gained between 3–5% on speculation that a longer-term mortgage option could expand lending activity.

Investors also see potential for mortgage-backed securities innovation, as Wall Street adapts to a new class of ultra-long-duration loans.

However, bond traders remain cautious. “Extending maturities to 50 years introduces new duration and prepayment risks,” said Jeffrey Sherman, deputy CIO at DoubleLine Capital. “It could take years for the market to price these properly.”

The Bottom Line

The idea of a 50-year mortgage reflects both the depth of America’s housing challenges and the Trump administration’s willingness to rethink traditional policy frameworks.

Whether it becomes a genuine solution or a political talking point will depend on how it’s implemented, and how markets respond.

For now, it signals one thing clearly: Washington knows the housing market can’t afford another decade of paralysis.

{kind=link}