Presidential Fed visits have long served as powerful symbols of confidence in the Federal Reserve’s independence and expertise. From Franklin D. Roosevelt’s post–Great Depression visits to Bill Clinton’s and Barack Obama’s walks through the Eccles Building, each appearance underscored a president’s respect for the Fed’s mandate. But Presidential Fed visits have taken on a sharply different tone with Donald Trump’s visit today, prompting questions about political interference and market implications.

Presidential Fed visits have traditionally been orchestrated under tight protocols to preserve the central bank’s apolitical stance. Roosevelt’s 1936 tour celebrated his New Deal partnership with the Fed to stabilize the economy. His successor, Harry Truman, quietly observed open market operations in 1947, signaling continuity in monetary policy. Decades later, presidents used these visits to bolster public trust, without intruding on rate decisions or internal deliberations.

However, today’s meeting between President Trump and Fed Chair Jerome Powell breaks from that tradition. Trump’s prior public criticisms of Powell, blaming him for slowing growth through higher interest rates, cast a long shadow. Rather than a neutral handshake, Presidential Fed visits now risk appearing as direct interventions in monetary policy.

A long tradition of endorsement

Presidential Fed visits first began as private tours. Roosevelt, wary of appearing to politicize monetary tools, kept his 1936 visit off the public stage. Over time, these tours became more transparent: John F. Kennedy’s 1962 stop highlighted collaboration in funding scientific research, while Jimmy Carter’s 1978 visit underscored the Fed’s role in taming rising inflation.

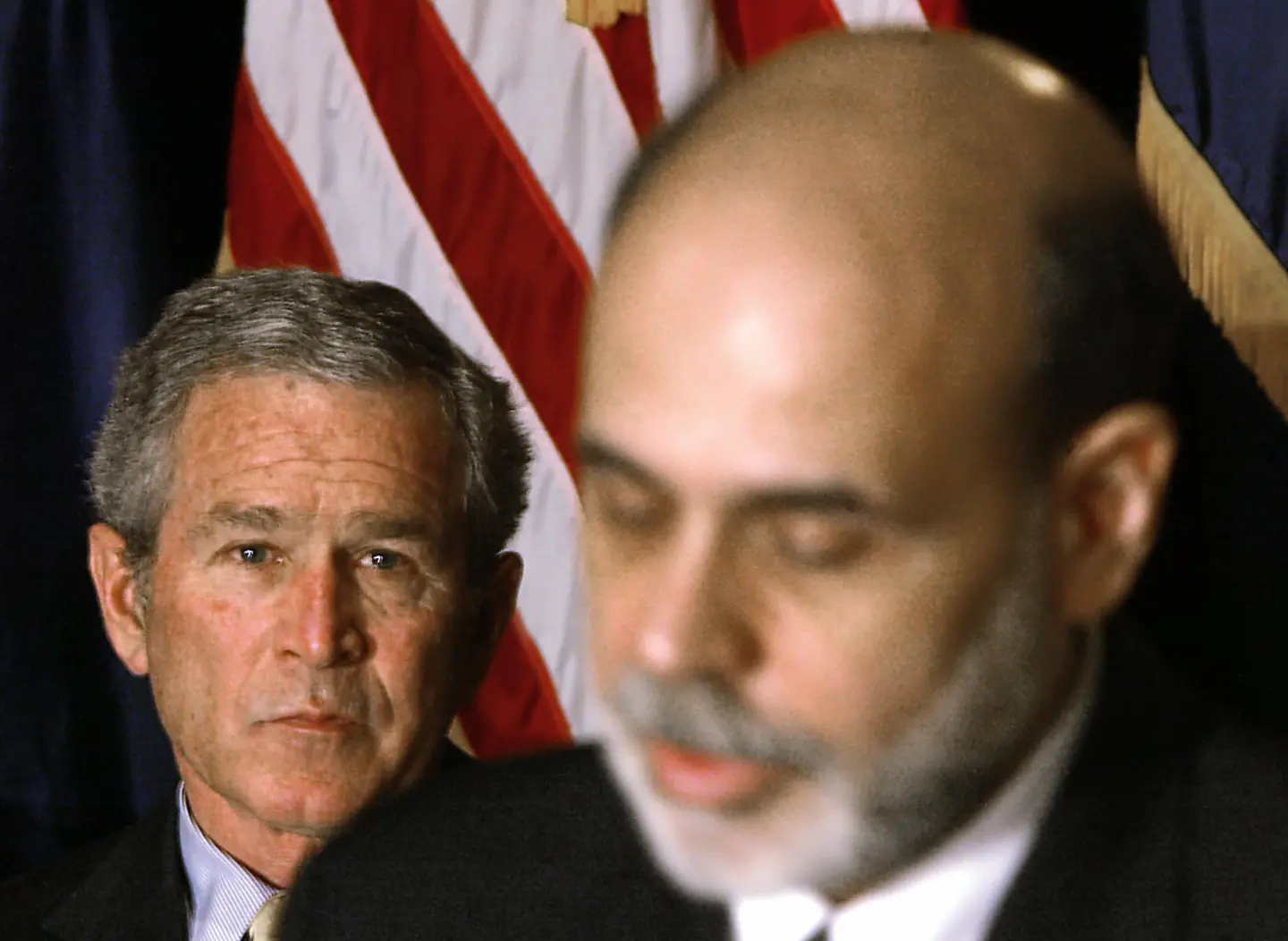

By the 1990s, presidents used these visits to communicate shared economic priorities. Bill Clinton praised the Fed’s independence even as he proposed fiscal measures to spur growth. George W. Bush, in 2005, thanked the Fed for judicious rate cuts post–dot-com crash, emphasizing mutual respect.

Obama’s affirmations of independence

During the 2008 financial crisis, Presidential Fed visits took on new urgency. President Obama’s 2010 visit was an explicit endorsement of Ben Bernanke’s emergency lending programs. “The Fed’s actions saved our economy,” Obama declared, thanking the Fed for acting without political pressure. That visit reinforced the principle that even in turmoil, the central bank must remain beyond partisan reach.

Trump’s visit – political theater or policy push?

In contrast, Trump has publicly chastised Powell more than a dozen times since assuming office, accusing him of undermining the economy to punish Trump’s policies. Today’s Presidential Fed visit, held on the eve of key inflation data, is widely viewed as a bid to influence rate decisions. Trump’s aides have hinted at seeking a more “growth-friendly” Fed leadership, reviving talk of replacing Powell, though most legal experts deem outright removal unlikely.

Markets reacted nervously to the announcement, with Treasury yields edging higher and equity futures dipping, a reminder that Presidential Fed visits can carry real economic weight when boundaries blur.

Why independence matters

The Fed’s design, an independent central bank with appointed governors, aims to shield monetary policy from short-term political aims. Numerous studies show that politicized rate decisions lead to higher inflation and weaker growth over time. By defending its autonomy, the Fed ensures that interest rate policy is driven by data, not election cycles.

Presidential Fed visits that stray from ceremonial goodwill risk eroding that autonomy. If presidents leverage these events to advocate for specific rate paths, investors may lose trust in the Fed’s commitment to its dual mandate: maximum employment and stable prices.

What’s next?

After today’s meeting, eyes turn to Powell’s post-visit remarks and the Fed’s upcoming policy statement. Will the Fed reassert its data-driven approach? Or will today’s unusual Presidential Fed visit mark the start of more overt White House involvement in rate decisions? The answer will shape financial markets and public confidence in the central bank for years to come.

{kind=link}